Australia's Surcharging Ban Starts October 2026. Here's How to Come Out Ahead.

Last updated: April 2026

You've probably heard about the surcharging ban. If you run a business that takes card payments (which is probably 90% of you), this one's for you.

What you might not have heard is that for you, this might actually be a good news story.

The Reserve Bank of Australia announced in March 2026 that surcharging on debit and credit cards will end from 1 October 2026. If you've been adding 1 to 2% on card transactions, that's going away. And if your first thought was "so I just absorb that cost now?" you're not the only one.

But that's not the full picture. And the full picture actually looks better than the headline suggests.

What's Actually Changing

The RBA isn't just banning surcharges. They're also cutting interchange fees (the fees your bank charges behind the scenes every time a customer taps their card). These are the biggest component of what you pay to accept card payments.

The new interchange fee caps are lower across the board, and small businesses are getting larger reductions than big retailers. On top of that, from April 2027, the RBA is introducing caps on foreign card transactions (which have historically been much more expensive) and requiring payment providers to publish their fees in a standardised format.

To put it simply: if businesses can't pass card costs on to customers anymore, the cost of accepting cards needs to come down too. And that's exactly what's happening.

For a lot of businesses, particularly those turning over $1M or more with a high volume of card transactions, the maths could actually work out in your favour. Lower interchange fees, no surcharge to manage, simpler checkout. That's a win.

But there's a catch.

Why the Surcharging Ban Alone Won't Save You Money

Lower interchange fees only help you if your payment provider actually passes the savings on.

And right now, there's no automatic mechanism that forces them to. The RBA is setting caps on what the banks can charge, but between the bank and your terminal, there's your payment provider's margin. If they keep their fees the same while interchange drops, they pocket the difference.

Our thoughts? This is where the real action is for business owners. The regulation is doing its job. But the benefit only reaches your bank account if you're paying attention to what your provider charges, and whether it moves when the caps change.

If you're currently surcharging 1.5% on, say, $500,000 of annual card payments, that's $7,500 a year you'll no longer collect from customers. Whether you absorb that or offset it with lower fees depends entirely on what happens between now and October.

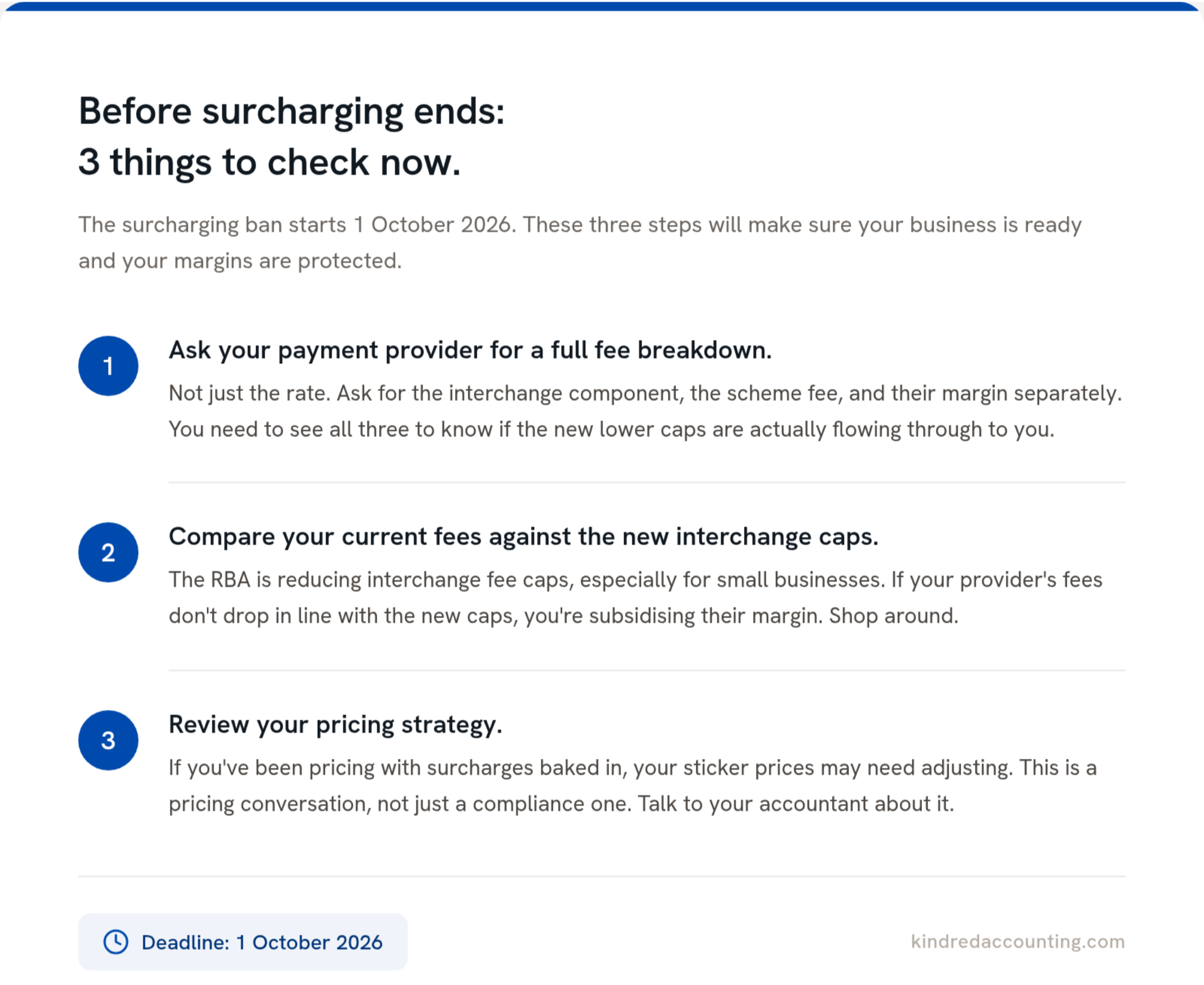

3 Things to Do Before October 2026

This is the practical bit. Three things to sort out before the surcharging ban kicks in.

Get a full fee breakdown

Your payment provider probably bundles interchange, scheme fees, and their own margin into one number. Ask them to unbundle it. You want to see the interchange component (what the bank charges), the scheme fee (what Visa or Mastercard charges), and your provider's margin separately. You need all three to know whether the new caps are actually flowing through to you.

Check the new interchange caps

Once you can see the interchange component, compare it to the RBA's new caps. If your provider's total fee doesn't drop roughly in line with the interchange reduction, you're effectively subsidising their margin. That's your cue to shop around. And with the new transparency rules coming in April 2027, comparing providers is about to get much easier.

Rethink your pricing

If you've been pricing with surcharges baked in, your sticker prices may need adjusting. This isn't just a compliance change. It's a pricing conversation. How do your margins hold without the surcharge buffer? Do you need to adjust menu prices, service rates, or quote structures? Talk to your accountant about it. (cough cough us)

What This Means for Your Business

For most business owners we work with, this change won't be the disaster the headlines make it sound like. The combination of lower interchange fees and no surcharging overhead will simplify things. Some businesses will come out ahead.

Others will come out roughly neutral.

The ones who come out worse are the ones who don't check. The ones who assume their payment provider will automatically adjust, or who don't revisit their pricing before October.

If you're reading this and already thinking about your numbers, that's a good sign. You're ahead of the curve.

Quick Answers

When does the surcharging ban start? 1 October 2026 for domestic debit and credit card payments. Caps on foreign card fees and new transparency rules follow from 1 April 2027.

Will my card processing fees go down automatically? Not necessarily. The RBA is lowering interchange fee caps, but your payment provider decides whether to pass those savings on to you. That's why step one is asking for a full fee breakdown.

Do I need to change my pricing? If you've been adding a surcharge at the point of sale, yes. You'll need to decide whether to absorb the cost (which should be lower with reduced interchange fees) or adjust your base pricing. It's worth running the numbers with your accountant before October.

What to Do Next

Want to run the numbers on how this affects your business? Whether it's a pricing review or a bigger conversation about your year-end position, that's what we're here for.